For years, innovation in FinTech was measured by what customers could see: sleek mobile apps, digital wallets, contactless payments, and intuitive user experiences. The competition centered on designing better interfaces and adding more financial features.

That mindset is changing.

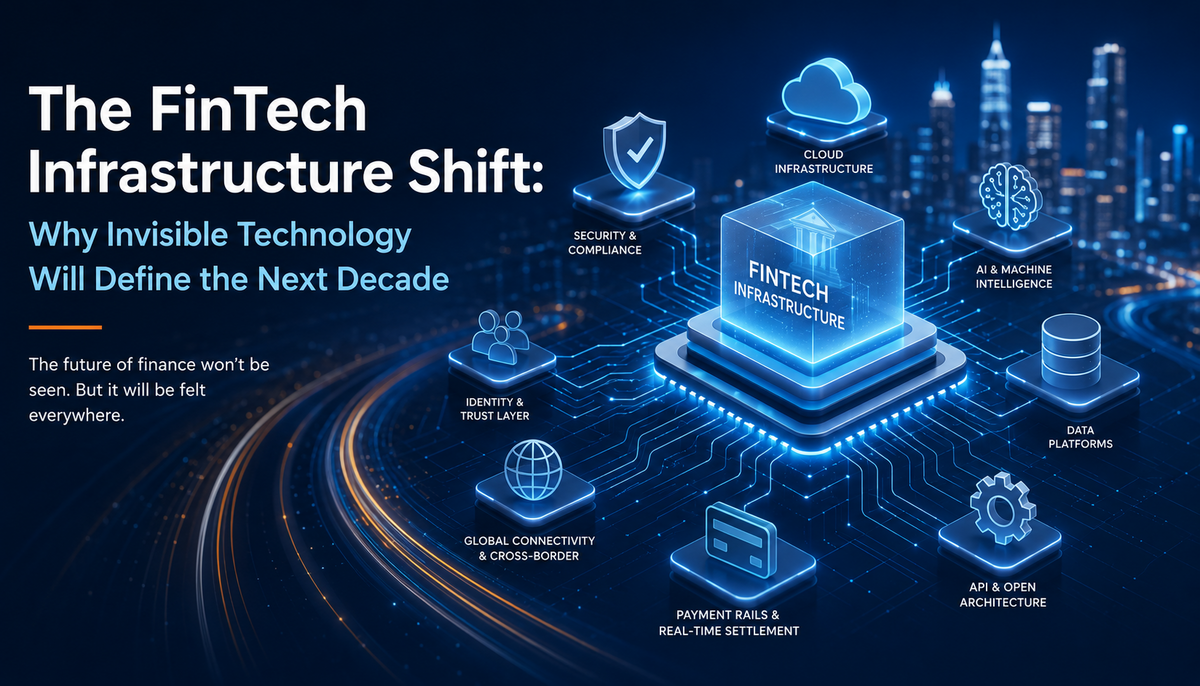

Today's biggest transformation isn't happening on smartphone screens—it's happening behind them. Financial institutions, payment providers, and enterprise businesses are investing in infrastructure that customers may never notice but will experience every time they make a payment, transfer money internationally, apply for financing, or interact with AI-powered financial services.

The next decade of FinTech won't be defined by the apps consumers use. It will be defined by the invisible technology powering them.

The New Competitive Advantage is Infrastructure

Modern financial services are becoming increasingly interconnected. Payments, identity verification, fraud prevention, compliance, treasury management, and cross-border settlements are no longer isolated functions. They operate as part of a continuously connected ecosystem where data, automation, and intelligence flow in real time.

This evolution is shifting investment priorities.

Instead of building another digital banking interface, organizations are modernizing payment rails, upgrading API architectures, adopting real-time data platforms, and integrating AI into financial operations. The objective is simple: create financial systems that are faster, more resilient, and capable of scaling without adding operational complexity.

Infrastructure has become the foundation of competitive advantage rather than an operational necessity.

AI Is Moving From Customer Service to Financial Operations

Artificial intelligence has already transformed customer support through conversational assistants and automated service interactions. The next phase reaches much deeper into financial operations.

AI is increasingly being used to monitor payment flows, detect fraud in milliseconds, automate reconciliation, optimize treasury decisions, improve underwriting, and strengthen regulatory compliance. Rather than replacing financial professionals, AI is becoming an operational layer that continuously analyzes data and supports faster, more informed decisions.

This operational shift is attracting significant investment. Global payments company Airwallex recently raised $320 million to accelerate AI capabilities alongside its international expansion, reflecting growing confidence in infrastructure-focused FinTech rather than purely consumer-facing innovation.

The emphasis is no longer simply on digitization. It's on intelligent financial infrastructure.

Payments Are Becoming Invisible

Consumers increasingly expect payments to happen instantly, regardless of geography, banking network, or currency.

Behind that expectation lies an enormous amount of infrastructure.

Real-time payment networks, API-driven settlement systems, cloud-native banking platforms, and programmable financial services are replacing slower legacy architectures. Businesses are also exploring tokenized assets and digital settlement mechanisms to reduce transaction costs and improve liquidity management.

Industry experts increasingly describe stablecoins not as speculative assets but as payment infrastructure designed to support faster settlement, cross-border commerce, and enterprise treasury operations. The long-term opportunity lies less in the digital currencies themselves and more in the platforms, compliance systems, wallets, custody services, and payment infrastructure supporting them.

The result is an ecosystem where payments become nearly invisible to the user while becoming significantly more sophisticated underneath.

Compliance Is Becoming Part of the Infrastructure

Financial regulation has traditionally been viewed as a separate operational function that followed innovation.

That sequence is changing.

As AI, digital assets, and embedded finance continue expanding, regulatory technology is increasingly being designed directly into financial infrastructure. Identity verification, transaction monitoring, fraud detection, anti-money laundering controls, and reporting capabilities are becoming embedded components rather than external processes.

Recent regulatory developments reflect this evolution. The UK has introduced updated stablecoin regulations designed to balance innovation with oversight, reducing some capital requirements while bringing digital payment infrastructure under clearer regulatory supervision.

Rather than slowing innovation, well-designed compliance infrastructure is becoming an enabler of enterprise adoption.

Embedded Finance Is Growing Beyond Payments

Embedded finance initially focused on integrating payment options into digital products.

Its scope has expanded considerably.

Businesses are now embedding lending, insurance, treasury services, foreign exchange capabilities, and financial analytics directly into software platforms. Instead of switching between multiple providers, organizations increasingly expect financial capabilities to exist within the applications they already use.

This trend is accelerating demand for infrastructure that connects banks, payment providers, enterprise software, AI agents , and regulatory platforms through standardized APIs.

The user experiences only a seamless transaction.

The complexity remains hidden beneath the surface.

The Rise of Autonomous Financial Systems

One of the most significant developments shaping enterprise FinTech is the emergence of autonomous financial operations.

Instead of simply generating reports, intelligent systems are beginning to recommend cash management decisions, automate reconciliation, optimize payment routing, forecast liquidity needs, and proactively identify operational risks.

While human oversight remains essential, financial workflows are steadily becoming more automated and predictive.

Industry forecasts increasingly point toward AI agents, embedded finance, and programmable payment infrastructure converging into what many describe as autonomous finance—a model where financial systems continuously monitor, analyze, and optimize themselves with minimal manual intervention.

For enterprise leaders, this represents more than another technology trend. It signals a fundamental redesign of financial operations.

Looking Ahead

The next decade of FinTech won't be remembered for a single breakthrough application or another digital wallet.

It will be remembered for the infrastructure that quietly transformed how money moves, how compliance operates, how AI supports financial decision-making, and how enterprises build connected financial ecosystems.

The most valuable innovations will often remain invisible to customers.

Yet those invisible systems-modern payment rails, intelligent automation, embedded compliance, real-time settlement, and AI-powered operational infrastructure,will determine which organizations deliver faster services, lower costs, stronger resilience, and greater trust.

In the coming years, FinTech leadership will be measured less by the features users can see and more by the infrastructure they never notice.